Despite slowing global trade, geopolitical tensions, and increasing uncertainty across major export markets, Vietnam posted GDP growth of 8.02 per cent in 2025, reinforcing its position as one of the world’s fastest-growing economies. The government has since set an ambitious target of at least 10 per cent growth in 2026 as it works toward becoming a high-income economy by 2045.

That growth story continues to resonate with foreign investors. According to the Business Climate Survey for Swedish Companies in Vietnam 2026, conducted by Business Sweden and the Embassy of Sweden in Vietnam, Swedish enterprises remain overwhelmingly positive about the country’s long-term prospects. Half of survey respondents plan to increase their investment over the next 12 months, while 61 per cent expect industry turnover to grow. Notably, none of the respondents expect to operate at a loss this year.

The findings highlight a market that continues to attract international businesses despite mounting global uncertainty. They also reveal a familiar challenge. While confidence in Vietnam’s future remains strong, investors continue to identify regulatory complexity, customs procedures, and administrative inefficiencies as the biggest barriers to growth.

For policymakers seeking to attract higher-value investment and move Vietnam further up the global value chain, that gap between opportunity and execution may become one of the country’s most important economic challenges.

Driving business optimism

Vietnam’s economic momentum has consistently exceeded expectations in recent years, and 2025 was no exception. The country’s 8.02 per cent GDP growth significantly outpaced forecasts from international organizations, many of which had projected growth closer to 6.5-6.8 per cent. The result underscored Vietnam’s resilience at a time when many export-oriented economies were struggling with weaker demand and heightened geopolitical risks.

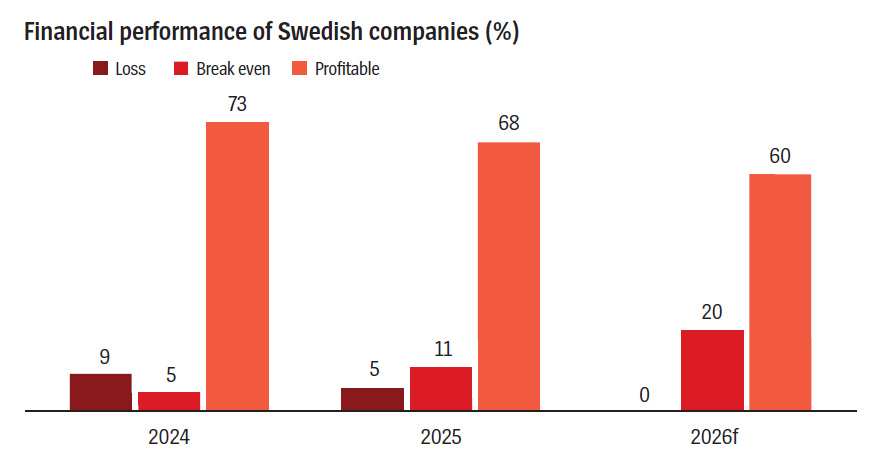

Swedish businesses operating in Vietnam appear to be benefiting from that resilience. Nearly seven in ten companies reported profitable operations in 2025, while an increasing number of firms moved from losses to break-even performance. Looking ahead, 60 per cent expect to remain profitable in 2026 and another 20 per cent expect to break even. No respondent expects losses this year.

The strongest performance came from consumer-facing companies. Though they accounted for just 21 per cent of survey respondents, every company in the sector reported profitability in 2025. That marks a dramatic turnaround from the previous year, when consumer businesses were the only segment reporting losses. Small companies also performed well, with 70 per cent reporting profitable operations.

The outlook remains positive, though slightly more cautious than in previous years. Among surveyed companies, 61 per cent expect turnover to increase over the coming year, compared with 81 per cent in the previous survey. At the same time, 21 per cent now expect turnover to decline, up from just 3 per cent a year earlier.

The shift does not necessarily signal weakening confidence in Vietnam itself. Rather, it reflects growing concerns about the broader global economy. International organizations, including the World Bank and the International Monetary Fund (IMF), have warned that slowing trade, geopolitical tensions, and policy uncertainty could weigh on growth across export-dependent economies.

Vietnam remains exposed to those risks. Yet compared with many regional competitors, it continues to enjoy several structural advantages, including strong manufacturing capabilities, expanding trade networks, and sustained foreign investment inflows. Those advantages help explain why businesses remain optimistic even as expectations become more measured.

New wave of investors

One of the most striking findings in the survey is how rapidly the profile of Swedish businesses in Vietnam is evolving. More than four in ten respondents established operations in Vietnam after 2020, making recent entrants the largest group represented in the survey. By comparison, only 24 per cent of respondents entered the market before 2004.

The trend reflects Vietnam’s growing importance within global supply chains. As multinational companies seek to diversify production and reduce dependence on single-country manufacturing hubs, Vietnam has emerged as one of the primary beneficiaries of “China+1” strategies. Competitive labor costs, political stability, a growing domestic market, and an extensive network of free trade agreements have all strengthened the country’s appeal.

The numbers suggest investors are responding. According to the National Statistics Office at the Ministry of Finance, disbursed FDI stood at approximately $27.6 billion in 2025, up 9 per cent year-on-year and the highest level recorded in five years. At the same time, Vietnam climbed from 73rd place in 2025 to 39th globally in the 2026 Global Opportunity Index, ranking second among Asia’s growth markets.

Among Swedish companies, confidence is translating directly into investment plans. Fifty per cent of respondents expect to increase investments over the next 12 months, while 29 per cent plan to maintain current levels. Only 11 per cent anticipate reducing investment. Larger companies appear particularly confident. Around 60 per cent of both large and medium-sized firms expect to expand investments during the coming year.

Yet the survey also reveals that many Swedish companies are still operating relatively small footprints in Vietnam. Though more than half of respondents belong to large multinational corporations globally, 78 per cent employ fewer than 250 people locally. Just 3 per cent have more than 1,000 employees in Vietnam.

That gap suggests significant room for future expansion. Many companies appear to be treating Vietnam not only as a manufacturing base but increasingly as a long-term growth market. The diversity of sectors represented in the survey supports that conclusion. Energy and electricity companies account for the largest share of respondents at 19.4 per cent, followed by consumer goods at 16.1 per cent. Business services, consumer services, healthcare and pharmaceuticals, and industrial equipment each account for nearly 10 per cent.

The prominence of the energy sector is particularly noteworthy. It reflects growing cooperation between Sweden and Vietnam in renewable energy, sustainability, and green transition initiatives. At the same time, the strong presence of consumer-focused companies highlights Vietnam’s growing role as a consumer market in addition to its traditional position as a manufacturing hub.

Bureaucracy remains a major obstacle

If there is one issue that consistently emerges throughout the survey, it is frustration with administrative processes. Despite strong optimism about the market, Swedish companies continue to rank customs procedures, licensing requirements, permits, approvals, and the financial system among the weakest aspects of Vietnam’s business environment.

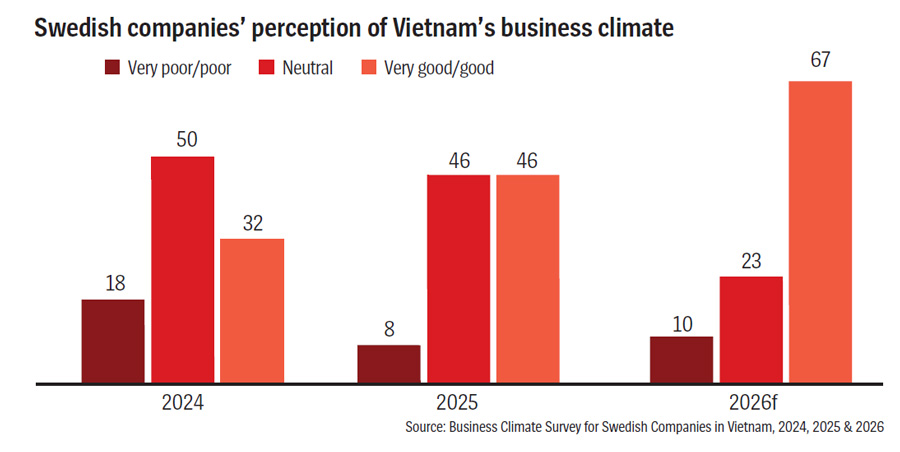

That finding stands in sharp contrast to the broader improvement in business sentiment. Sixty-seven per cent of respondents now describe Vietnam’s business climate as good or very good, up from 46 per cent in the previous survey. Meanwhile, the share of neutral responses has fallen significantly, while only 10 per cent view the business environment negatively.

Companies also report high levels of satisfaction with distributors, suppliers, and personal safety. Access to local distribution networks and supplier relationships improved notably compared with previous years, reinforcing Vietnam’s reputation as a reliable operating environment for international businesses.

The survey suggests that Vietnam’s next stage of competitiveness may depend less on labor costs and more on institutional efficiency. Sustainability offers a clear example of this shift. Nearly 60 per cent of respondents say environmental considerations play an important role in customers’ purchasing decisions. At the same time, Swedish companies recognize significant opportunities linked to Vietnam’s commitment to achieve net-zero emissions by 2050.

However, many respondents also believe progress has not kept pace with ambition. Regulatory reforms and clearer implementation frameworks will likely be necessary to accelerate investment in green technologies, renewable energy, and sustainable infrastructure.

The survey’s overall message remains positive. Vietnam remains one of Asia’s most attractive investment destinations. Strong economic growth, rising foreign investment, expanding supply chains, and growing domestic demand continue to create opportunities across multiple industries. But economic growth alone will not be enough to sustain momentum indefinitely.

To unlock the next wave of investment, Vietnam will need to address the administrative bottlenecks that continue to frustrate companies already operating in the market. Streamlined procedures, greater regulatory transparency, and more efficient approvals could help transform strong investor interest into larger commitments and deeper market expansion. For now, Swedish companies remain committed to Vietnam’s future. The question is whether regulatory reforms can keep pace with the country’s economic ambitions.

Google translate

Google translate