Vietnam’s consumer economy is entering a new phase. While the country recorded around 8 per cent GDP growth in 2025 and officially joined the ranks of upper-middle-income economies, consumer spending patterns are becoming increasingly complex. Rising incomes are no longer translating automatically into higher spending on everyday household goods, as consumers redirect more of their budgets toward experiences, travel, dining, and products that offer clear lifestyle benefits.

These shifts are highlighted in Worldpanel by Numerator’s Vietnam FMCG [fast-moving consumer goods] Outlook 2026 report, which paints a picture of a market undergoing structural change. Beneath the headline economic growth figures, the report points to a more cautious and selective consumer, growing fragmentation across demographic groups, and intensifying competition for consumer attention.

For brands seeking growth in Vietnam, understanding these changes may prove just as important as understanding the country’s macro-economic performance.

From optimism to spending caution

Vietnam’s economic fundamentals remain strong. According to the report, average monthly income per capita reached VND5.9 million ($227) in 2025, representing annual growth of around 7 per cent over the past five years. Manufacturing, services, transportation, and hospitality all recorded robust expansion, supported by strong domestic demand and a busy calendar of national celebrations and public events.

Yet despite these positive indicators, Vietnamese consumers continue to approach spending decisions carefully. Research cited in the report shows that concerns about food safety, product authenticity, rising food prices, and job security remain among the most significant issues facing households. High-profile investigations into counterfeit and sub-standard goods throughout 2025 have also heightened public awareness over product quality, making consumers more cautious when selecting brands and products.

This growing scrutiny is reshaping purchasing behavior. Rather than simply seeking affordable products, consumers increasingly want reassurance that products are safe, reliable, and worth the money.

At the same time, government efforts to tighten controls on counterfeit goods and strengthen regulatory oversight are helping create a more transparent marketplace. While this raises compliance requirements for businesses, it may also benefit established and legitimate brands by increasing consumer trust in formal retail channels.

Beyond the home

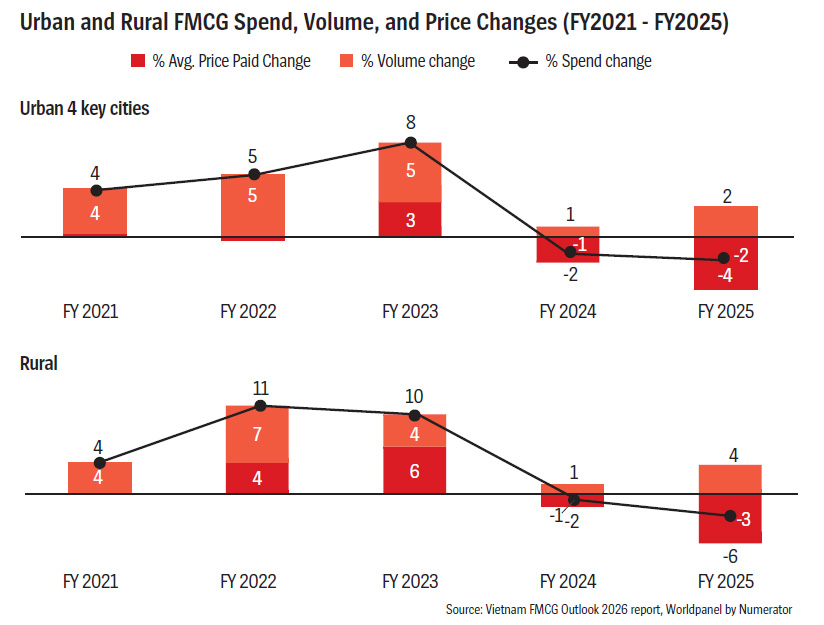

One of the report’s most notable findings is the divergence between overall consumer spending and in-home FMCG consumption. Household FMCG volumes declined in both urban and rural Vietnam during 2025, with rural areas experiencing particularly pronounced contraction. The slowdown suggests that consumers are purchasing fewer traditional household products despite enjoying higher incomes.

However, this does not mean consumers are spending less. The report highlights strong growth in Vietnam’s broader food and beverage sector, where revenues are projected to increase by almost 10 per cent in 2025. Domestic tourism also reached a record 135.5 million trips, reflecting a growing appetite for travel, entertainment, and social experiences.

Together, these trends point to a fundamental shift in consumption priorities. As living standards improve, consumers are allocating a greater share of their discretionary spending toward activities outside the home.

For FMCG companies, this presents a challenge. Growth can no longer be taken for granted simply because incomes are rising. Brands must increasingly compete not only against rival products but also against alternative uses of consumers’ time and money.

The impact is particularly evident in food and beverage categories. Dairy products, packaged foods, and beverages have experienced some of the sharpest volume declines, influenced by changing consumption occasions, food safety concerns, and evolving consumer preferences.

Rise of selective consumers

Though many traditional categories are under pressure, the report also identifies several areas of opportunity. Products associated with convenience, beauty, health, and self-care continue to outperform the broader market. Categories such as lip care, sun protection, foundation cosmetics, deodorants, multipurpose cleaners, and convenient meal solutions have shown stronger momentum than staple food and beverage products.

The trend reflects the emergence of a more sophisticated consumer mindset. Rather than increasing consumption across the board, shoppers are concentrating spending on products that align with their lifestyles, save time, or support personal wellbeing.

This shift helps explain why some smaller brands are gaining market share at the expense of industry leaders. According to the report, nearly two-thirds of FMCG categories have recorded notable market-share declines among their three largest manufacturers.

Smaller brands are often proving more effective at addressing niche consumer needs, responding quickly to emerging trends, and communicating differentiated value propositions. In an environment where consumers are more selective, relevance can become a stronger advantage than scale.

Fragmented consumer landscape

Behind these changes lies a deeper demographic transformation. Vietnam’s population surpassed 102 million in 2025, but the country’s consumer story is increasingly defined by changes in household composition, age structure, and income distribution rather than population growth alone.

The report highlights several long-term shifts, including declining fertility rates, continued urbanization, rising incomes, and a rapidly aging population. By 2036, Vietnam is expected to officially become an aging society.

At the same time, smaller households are becoming increasingly common. Families with three members or fewer now account for nearly half of all households nationwide. These households tend to spend differently from traditional larger families. Convenience, premiumization, self-care, and lifestyle-oriented purchases play a larger role in their spending decisions, creating opportunities for brands capable of understanding their specific needs.

As a result, broad demographic categories are becoming less useful as marketing tools. The future belongs to what the report describes as “micro consumer clusters” - highly specific groups defined by age, income, lifestyle, family structure, and purchasing motivations.

For businesses, this means growth strategies will need to become far more targeted than in the past. Vietnam remains one of Asia’s most promising consumer markets. Economic growth is strong, incomes are rising, and consumer spending continues to expand. But the nature of that spending is changing.

The era of broad-based FMCG growth driven by rising incomes and population expansion is giving way to a more nuanced market, where success depends on understanding increasingly diverse and selective consumers.

For brands looking ahead, the challenge is no longer convincing Vietnamese consumers to spend. It is convincing them that their products deserve a place in an increasingly competitive battle for attention, trust, and wallet share.

Google translate

Google translate